Pitfalls and Lessons learnt: By Dr. Harish Kotadia, Ph.D.

Our team delivered an agentic auto loan origination program on Claude. The biggest risk on the plan was never the model. When reflecting on this project, the team discovered unique challenges specifically relevant to managing a Claude auto loan system.

It was scope.

We had a genuinely hard model problem, a regulated credit decision, and integrations with three bureaus. The thing that nearly derailed us was a quiet, reasonable-sounding request: “just let the model decide the easy cases.”

This is a delivery story, not an architecture one. Here are the six pitfalls that cost us the most, and the lesson we took from each. The pattern across all of them: the model was the easy part.

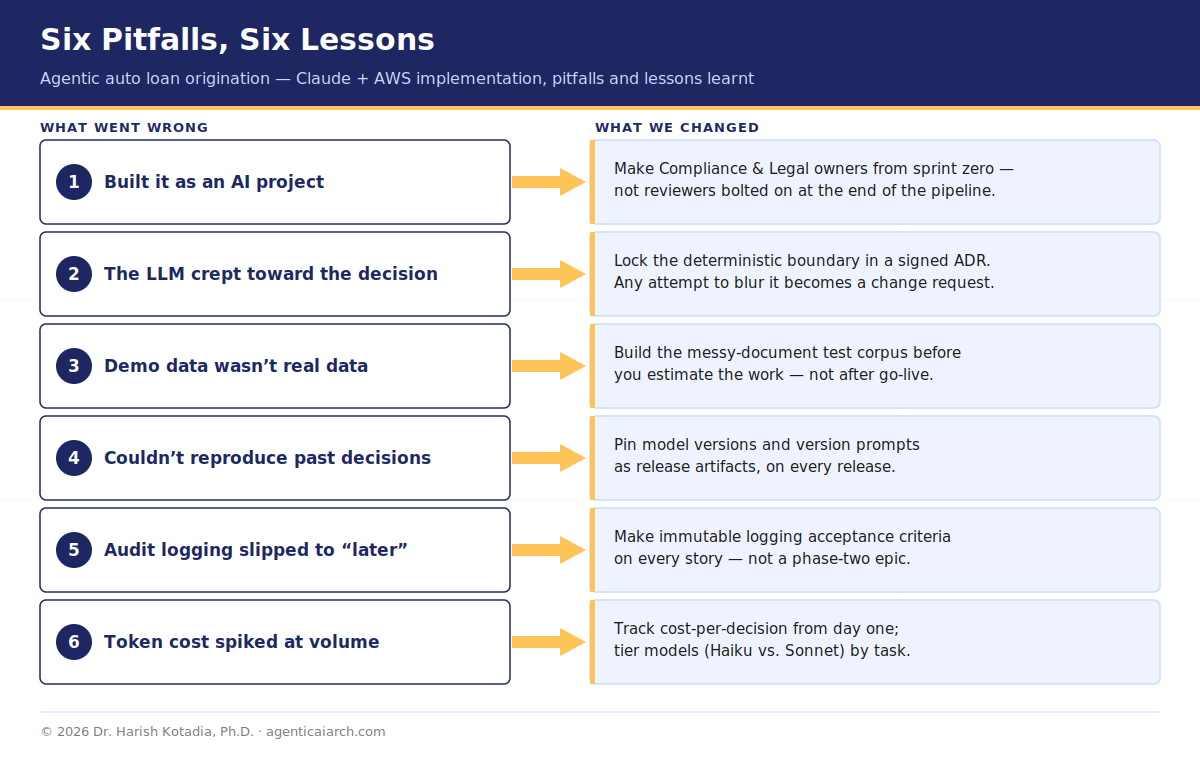

1. Run it as a lending program, not an AI project.

Pitfall: we first scoped it as an AI build, with compliance review at the end of the pipeline. That order is backwards in regulated lending. With initiatives like a Claude AWS auto loan, reversing this order means greater risk.

We made compliance and legal owners on the RACI from sprint zero. Adverse-action language, prohibited-basis rules, and audit requirements became acceptance criteria before the engineers built anything against them. It removed an entire category of late rework.

2. Make the decision boundary a contract, not a preference.

Pitfall: the model kept creeping toward the decision, one “easy case” at a time.

We wrote the boundary into an architecture decision record on day one: the model never makes the lending decision. A validated deterministic engine decides. Claude reads documents, reconciles income, retrieves policy, and drafts the rationale — it proposes and explains, it does not decide. Once it was a signed ADR, every attempt to blur the line became a change request with a compliance sign-off attached. This kind of contract is essential for any auto loan automation project involving Claude and AWS elements together.

3. Estimate against real documents, not the demo.

Pitfall: the demo ran on clean pay stubs; production handed us scans and layouts we had never modeled.

Real documents broke our extraction, and we had estimated against the easy version. We rebuilt the test corpus from real, messy documents and re-baselined. We now treat a representative document set as a prerequisite to estimating, not an output of building. For future Claude AWS auto loan development, using actual samples will give much more reliable results.

4. Engineer for reproducibility from day one.

Pitfall: prompts evolved, a model version rolled, and for a short window we couldn’t cleanly reproduce why an earlier case landed where it did.

In regulated lending that’s an audit finding waiting to happen — “why was this loan declined last March” has to be answerable a year later. We pinned model versions and versioned prompts as release artifacts. Systems like a Claude AWS auto loan process must be designed with full auditability in mind.

5. Treat audit logging as acceptance criteria, not a later epic.

Pitfall: immutable logging kept slipping to “phase two,” because it never blocked a happy-path demo.

In a regulated decision, the log is the product. We made immutable capture of every prompt, response, retrieved policy chunk, tool call, and rationale acceptance criteria on every story that touched a decision. The demo reasons impressively; the system survives an audit. Only the second one ships. Building a Claude AWS auto loan workflow means logging from day one is crucial for success.

6. Make cost-per-decision a first-class metric.

Pitfall: per-loan token cost looked trivial in testing and surprised the whole room at production throughput.

We made cost-per-decision a tracked metric from the first integration test, and tiered the work — lighter models for extraction, the stronger model only where the reasoning needed it. In the context of a Claude AWS auto loan program, tracking these costs early reduces future surprises.

What we’d tell the next program team.

Book your SMEs as named dependencies. Underwriters and compliance officers have day jobs, and an agentic build needs more of their time, not less. Managing a Claude AWS auto loan implementation means you will coordinate with these experts a lot.

Calibrate the human-in-the-loop thresholds with those underwriters early. Route too much and you bottleneck the queue; route too little and you ship decisions nobody validated.

And resist the request to let the model do a little more than the boundary allows. It always sounds harmless. In a regulated decision, harmless is exactly how scope creep arrives. This advice applies directly to any Claude AWS auto loan deployment.

© Dr. Harish Kotadia, 2026. All Rights Reserved.

Dr. Harish Kotadia, Ph.D., is an Enterprise AI Architect with 20+ years of IT consulting experience serving Fortune 100 clients, specializing in agentic AI systems built on Anthropic Claude, AWS Bedrock, and Google Vertex AI. He holds a Ph.D. in Marketing Management with doctoral research in marketing analytics. Follow him at @agenticaiarch on X and at AgenticAIArch.com.